Today’s the day – for the first time since 2010, interest rates are going up. Pretty rare for the RBA to move rates in the middle of an election – and of course, both sides of politics are talking utter BS about their impact on rates (as usual!!). And no, Clive Palmer doesn’t have any ability whatsoever to keep rates below 3%, nor is it likely that either Labor or Liberal will have a better chance than either of controlling rates between now and the next election.

So – what next?

A few weeks ago, we posted that the horse had already bolted with fixed rates. Following that, it’s become apparent that there are a few questions about both fixed and variable rates, so here are a few answers from us.

Variable Rates – how fast & far will they go up – and when will they come back down?

Depends. Let’s grab the crystal ball… Hmm, can’t find one… Honestly, it’s anyone’s guess – and anyone who gives you a definitive answer is talking utter BS.

They’ll go up until the RBA is satisfied that inflation is under control. My bet (and that of many others) is that we’re not going back to 7% home loans – thanks to the latest rampant property boom, households have too much debt relative to their incomes to stomach rates that high.

Discretionary spending would drop off too much well before rates get that high, in turn sending us into a recession (and it’s that negative growth that generally causes interest rates to go down).

How much inflation is global vs local (i.e. whose fault is it)? A bit of both – the whole world was supercharged with cash as governments responded to COVID, then there’s Russia/Ukraine. Locally, sorry, but the Libs do have to cop some blame – it’s very easy to argue that they over-primed the economy with the cash splashing (JobKeeper, CashFlow Boost, HomeBuilder) – which in turn drove demand, which equals higher prices (that’s Economics 101).

When will they come back down? Sorry to be the bearer of bad news, but rates won’t go back down until the economy hits another roadblock if the RBA does their job right. They’ll plateau rates at just the right point if they get it right.

Fixed Rates – a bit more background to the horse that bolted

We’ve been seeing some chatter out there about banks profiteering by driving rates up – which made it apparent to us that there is a lack of understanding of how banks/lenders come up with rates, so we thought it might be valuable to provide some brief facts.

The RBA cash rate is only an overnight rate. Ultra short term. The over-simplified story is that when a bank has excess holdings at the end of the day, it can hand it to the RBA and get paid the cash rate for that money or pay that rate if it has too little. But that doesn’t equate to proper capital raising – they can’t decide they’re going to increase their home loan book by a billion dollars and borrow it from the RBA at that rate.

If they want to build their loan book, the two primary sources are (1) customer deposits (term deposits and everyday accounts) or, (2) borrowing from Institutional players in the wholesale market.

Banks set their own term deposit and bank account rates (that’s just a competitive market), which tends to be the preferred way, but most banks can only fund a proportion of their loan book this way. Some can’t fund any because they don’t offer deposit products.

The wholesale market… Ok I’ll try to keep this simple because it’s way more complex than I could explain here…

Let’s say you’re a company getting a loan from a bank. If you’re a good risk, you get a good rate; bad risk, high rate. The same goes for banks/lenders on the wholesale market… If I’m an institutional investor, it’s safer for me to lend to a major bank than it is to lend to a little low-doc lender. So, those two lenders pay different rates for their money. They then put a margin on that wholesale money, resulting in the retail rate paid by your retail borrower.

Now as a lender, you want to offer variable and fixed rates to your borrowers. To manage your risk, you want to roughly match the loans you provide to borrowers, with your wholesale funding sources. If a bank has a billion in loans on a three year fixed rate, it wants to lock away a billion of wholesale 3-year money.

So how this works in practice, is that every day/week/month (depending on the size of the institution and how much in loans they’re writing), a bank/lender will look at what they’ve written and then go to the wholesale market to lock in their cost of funds. If they wrote $500m in 3yr and $200m in 5yr fixed rates, they’d lock about those same amounts & terms on the market.

Similarly, their variable rate book will largely be left on short-term borrowing on the wholesale market (net of what they funded from customer deposits, and also balancing longer-term bonds… but I’ll gloss over that for simplicity’s sake!).

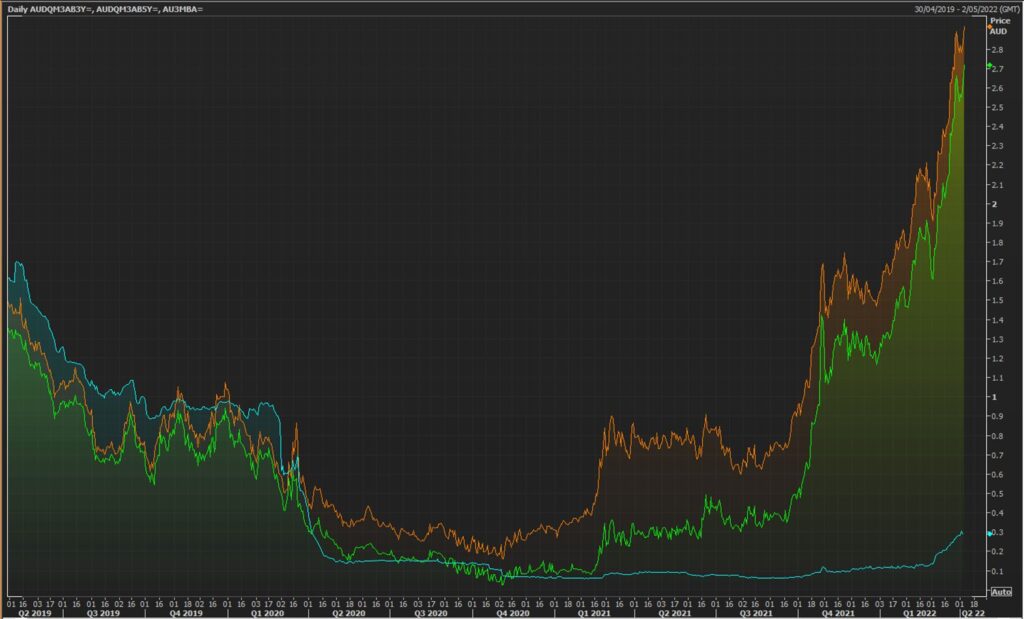

Bringing this to a close, as to why fixed rates have shot up so much lately… Attached is a screenshot from the wholesale market a few weeks ago (which we posted on LinkedIn). Blue Line is 90-day money; green is three years, orange is five years.

Those numbers are the genuine wholesale market prices. Adjustments are made to that depending on the borrower’s credit risk (I.e. the bank/lender), but you get the idea – this is the no BS wholesale market price.

This is why home loan fixed rates have shot up so much. The market is genuinely a good 2.5% or so above the short term (variable) rate.

Banks aren’t profiteering from this; they will be roughly maintaining their margins – the horse has bolted on the market because institutional investors genuinely believe rates are up a fair bit.

- Your full financial needs and requirements need to be assessed prior to any offer or acceptance of a loan product.

- STAC Home Finance Pty Ltd (534124) is authorised under Australian Credit Licence 389328.

- Click here to read our Privacy Policy.