I’ve been wondering something lately and have asked this question to a few people – then this morning I open a Bloomberg article that talks about some outlier economists asking the same question (so I can’t be completely crazy):

ARE INTEREST RATE MOVEMENTS NOW DOING THE OPPOSITE OF WHAT WE ASSUME THEY DO??

The RBA only has One Tool

The RBA’s tool belt is pretty light. They only have one tool – an interest rate hammer. Ask any mainstream economist and they’ll agree it’s limiting having only one blunt tool, but they’ll also probably say it works pretty well.

The simple theory is that most consumers and businesses have more debt than they have savings. Therefore, when the economy is too hot and inflation too high, the central bank pushes up interest rates, which causes consumers and businesses to have less disposable income to spend on stuff, in turn cooling the economy.

But what if that theory is no longer right…?

Baby Boomers Benefit from Rising Rates & Rents

With a rapidly ageing population (here and all around the world), a very large percentage of baby boomers are now in retirement – and the vast majority of them probably don’t have any debt anymore.

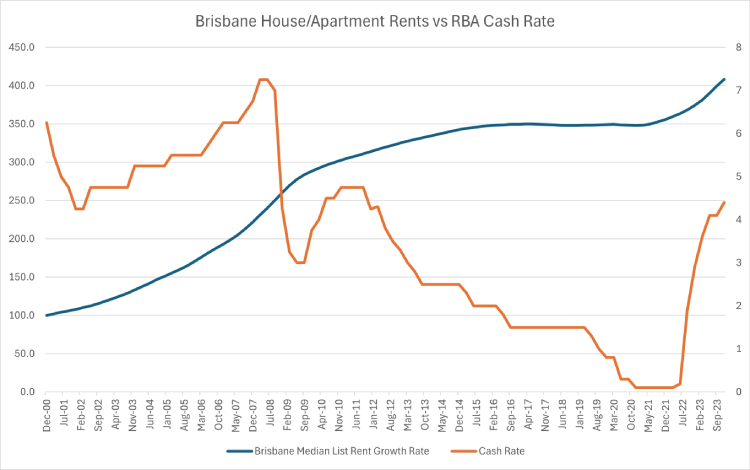

Conversely, they have cash in the bank – and of course a lot probably own rental properties. With rising interest rates, both of these asset classes (cash and property) have been enjoying rising income – just look at this recent spike in both:

Source: ABS, RBA, 2024

The thing I’m starting to wonder, is whether there’s a half-reasonable possibility that there are now so many cashed-up people in the population that are shouting out: “you little ripper, come in spinner! Beryl, let’s go out to dinner, we’re earning yet more interest, and our agent just put the rent up on all our houses!!” that are BENEFITING from rate rises, that official interest rate rises might actually starting to have the complete opposite effect to what the RBA and mainstream economic theory assumes?

More and More Renters (who don’t have Loans)

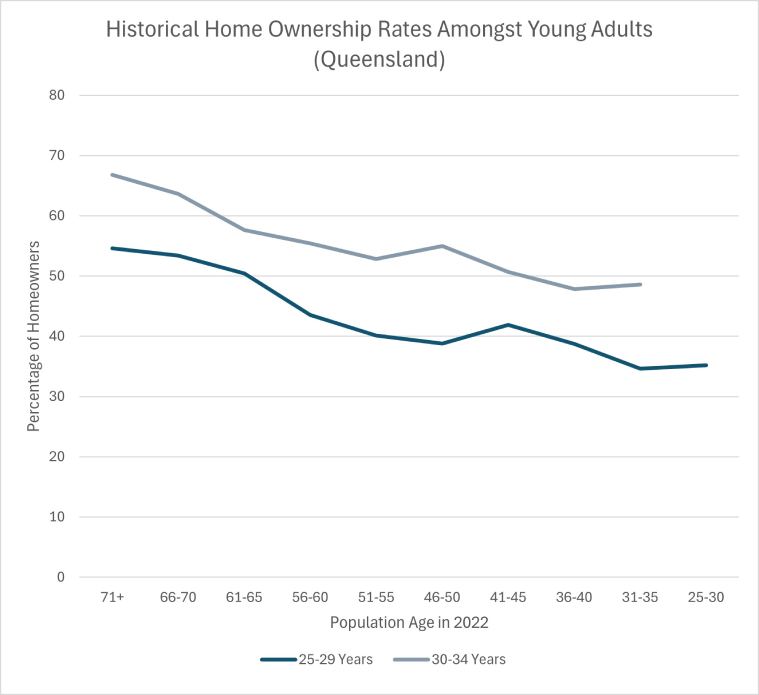

Here’s another interesting factor to consider. Driven by lower home affordability [although some have argued a greater love for Avo on Toast!], home ownership in the under-30’s age group is at record lows.

As this graph shows, some 55% of people who are now in their 70’s owned a home before they turned 30 (and nearly 70% did before they turned 35).

Some 40 years later, only about 35% of people under 30 have managed to buy their own home, and still less than half of under 35’s have bought.

Source: AIHW, 2023

That increasing percentage of renters don’t have home loans – and therefore, increasing interest rates aren’t directly affecting them. Add this part of the population to the first cashed-up group, there seems to be a rapidly decreasing percentage of the population who have big painful loans.

There is an argument that there is an indirect effect on renters though, because as interest rates go up, their landlord might need to cover their increased interest bill (assuming they have a home loan). But that’s definitely not a perfect correlation; supply & demand is far more of a driver of rents (although someone needs to teach the Greens Party that Economics 101 lesson…!!).

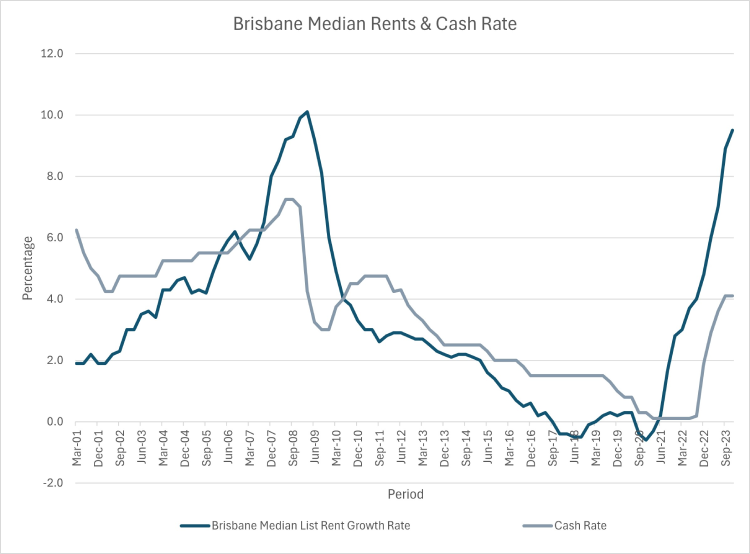

To help prove that point, here’s a graph of Brisbane residential rents over the last 20-something years, versus RBA cash rate:

Source: ABS, RBA, 2024

What’s that flat-spot from 2016 til COVID? Remember that apartment development boom we had in SE Qld, which over-supplied the market, followed by a softer local economy versus Sydney and Melbourne (and house prices that lagged a long way at that time!)? Lots of properties to rent, more than the number of renters – that’s what keeps rents under control.

Whilst a landlord might WANT a higher rent when their interest rates go up, if there’s too many rentals on the market, then rents don’t go up. It’s the lack of supply relative to demand that drives prices up.

Which is, of course, exactly what the majority of Australia is experiencing today.

Enter the Contrarians on Wall Street

This week, a Bloomberg article considers the same question – an excerpt:

As the US economy hums along month after month, minting hundreds of thousands of new jobs and confounding experts who had warned of an imminent downturn, some on Wall Street are starting to entertain a fringe economic theory.

What if, they ask, all those interest-rate hikes the past two years are actually boosting the economy? In other words, maybe the economy isn’t booming despite higher rates but rather because of them.

It’s an idea so radical that in mainstream academic and financial circles, it borders on heresy — the sort of thing that in the past only Turkey’s populist president, Recep Tayyip Erdogan, or the most zealous disciples of Modern Monetary Theory would dare utter publicly.

But the new converts — along with a handful who confess to being at least curious about the idea — say the economic evidence is becoming impossible to ignore. By some key gauges — GDP, unemployment, corporate profits — the expansion now is as strong or even stronger than it was when the Federal Reserve first began lifting rates.

This is, the contrarians argue, because the jump in benchmark rates from 0% to over 5% is providing Americans with a significant stream of income from their bond investments and savings accounts for the first time in two decades. “The reality is people have more money,” says Kevin Muir, a former derivatives trader at RBC Capital Markets who now writes an investing newsletter called The MacroTourist.

These people — and companies — are in turn spending a big enough chunk of that new-found cash, the theory goes, to drive up demand and goose growth.

…Eigen has two side hustles outside of JPMorgan. He runs a fitness center and car repair shop. At both places, people keep spending more money, he says. Retirees, in particular. They are, he notes, perhaps the biggest beneficiaries of the higher rates.

“All of a sudden, all of this disposable income accrues to these people,” he says. “And they’re spending it.”

Sounds like a pretty similar story to what’s happening here in Oz.

Insatiable Demand for Luxury Housing in Australia

At STAC, we now have a long list of home-builder clients, Activates Construction as just one example, building very nice luxury homes in inner-ring Brisbane suburbs, at prices generally ranging from $2.5 to 5m – a price bracket that only a few years ago was a pretty thin market for the top 5% of the population – and the demand is absolutely insatiable.

These aren’t prices of the traditional uber-wealthy suburbs anymore – these prices are regularly being achieved in suburbs that, only a few years ago, were considered to be pretty standard family suburbs.

Then there’s the homes you see being sold by the likes of GRAYA – uber-luxury in the $5-10m range, as well as countless large luxury apartment projects now regularly selling at higher prices than houses (and certainly far greater on a $ per square metre basis!), selling at this range and beyond. It seems to defy belief just how many people can spend this much money on their family home – even amidst elevated interest rates.

Much Tougher for the “Little Aussie Battler…”

The flipside of the coin is that there are millions of Australians currently under severe mortgage or rent stress, thanks to higher interest rates combined with elevated record-high house prices and an extreme lack of supply relative to demand, which is going to get worse before it gets better.

Unfortunately, these people are exactly what basic economic theory intends to do with central bank interest rates – to squeeze the population into spending less money, thereby cooling the economy.

The extreme lack of supply relative to demand is only going to get worse, before it gets better. For all the garble that every level of government has been coming out with lately about what they’re doing to help tame house and rent prices, the problem is all too obvious for those in the property development industry – in particular:

- Labour Supply (and the unions are making sure that the government doesn’t let construction workers immigrate!)

- Labour Cost (which is directly impacted by #1)

- Local Government ineptitude (try getting a DA for just about anything, anywhere, then tell me how much of an effort your local council is putting into solving housing affordability and supply!)

On the ground at STAC Capital, we can certainly attest to there being no end in sight to solving the affordable housing crisis. The vast majority of residential projects we’re funding, are high-end.

Make no mistake – developers DO want to build affordable housing en-masse – but it is extremely difficult to get an affordable project’s feasibility to stack up. Irrespective of whether you’re building a $500k apartment or $5m penthouse, the concrete and steel costs the same, the tradesmen knocking it all together charge the same – it’s really just the shiny stuff you see (a relatively small percentage of total cost) and the land value (very very high everywhere!) that are the price variables.

So, do Interest Rate movements actually work anymore?!

Is more of the population actually now benefiting to a greater extent from rate increases, than those who are feeling a financial squeeze on their big mortgage?

Is the interest rate hammer still doing what every economist takes for granted that it should do?

Or, are rate increases actually pumping MORE money INTO the system?

I’m not YET saying that is definitely the case, but it seems like the tide is turning.

But I’ll make the call here and now that, as the population ages more and more over the coming years, that coin is flipping.

What do you think?